Activity-based budgeting

The rise of e-commerce, globalisation, and shorter product life-cycles are some of the factors increasing competitive rivalry across many business sectors. Also, indirect costs are becoming a higher percentage of total costs for many companies as technology and automation investments become more crucial to success. Because of this, managers need a deeper and more accurate understanding of the true cost of delivering their goods or services. Activity-based budgeting (ABB) is a tool that helps with this and is closely linked to activity-based costing (ABC), also in your syllabus.

Under an absorption costing system, indirect costs are pooled together and labelled ‘overheads.’ An overhead absorption rate is then calculated, based on a single driver – for example, direct labour hours (which can be easily found via payroll records). Overheads are then assigned to products on the basis of the overhead absorption rate and direct labour hours per unit. This cost per unit can then be used for the budgeting process.

ABB, in conjunction with ABC, focuses on understanding how overheads are consumed by the production process. Overheads are analysed, and ABB then looks at costs from the perspective of the activities that are required to satisfy the customer. Production and non-production activities are measured and quantified, and then a cost per activity (or cost per driver) is determined through detailed analysis of operations and costs. Once the cost per driver is calculated, managers can then create a more accurate budget based on departmental consumption of activities. ABB is essentially ABC in reverse.

Pros and cons

During an ABB/ABC exercise, ‘non-value adding’ activities can be identified – these are activities which do not increase the customers’ perceived worth of the final product. These activities can then be eliminated. Value-adding activities and processes can then be automated or improved. Also, the budgeted costs and profit per product should be more accurate as costs per driver are determined after detailed analysis. ABB helps align value-added activities with objectives, reducing costs in the process.

However, there can be some disadvantages to using ABB. As stated above, ABB will require detailed analysis of overheads and measuring of activities. This can be a complex, costly and time-consuming project. If direct costs are more significant than indirect costs, and if the product range is narrow, the costs might outweigh the benefits of switching to ABB.

ABB example

Toy Co manufactures toys for toddlers and children. They are a small company and have a good reputation for producing high quality, innovative products. Their profit margins have been consistently higher than competitors in the same industry.

However, profitability has been slowly dropping over the past two years due to increasing overhead costs and the loss of several key customers because of shipping errors and missed delivery dates. The management accountant believes there are non-value added activities which can be removed to improve efficiency and reduce costs, and is considering the introduction of activity-based budgeting. He has decided to initially analyse two popular products, the ‘Tod’ and the ‘Kid’.

Much of the production process is automated and occurs in batches. Orders are placed by large retail chains and demand is relatively constant during the year.

Operational information for each product is as follows:

|

Tod |

Kid |

Quarterly demand (units) |

30,000 |

36,000 |

Production batch size (units) |

3000 |

1000 |

Order size (units) |

150 |

120 |

Information for the quarter:

|

Hours required |

Total Hours available |

Quality inspection time |

15 per batch |

860 |

Packaging and shipping time |

1 hour per order |

460 |

Requirement:

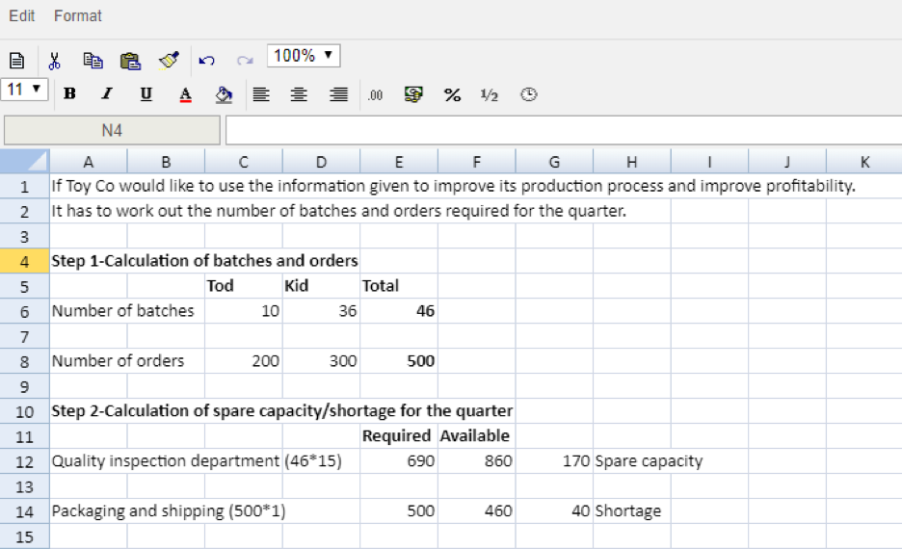

(a) Calculate the hours required for the next quarter and whether there is any spare capacity or shortage in the hours for:

- Quality inspection

- Packaging and shipping

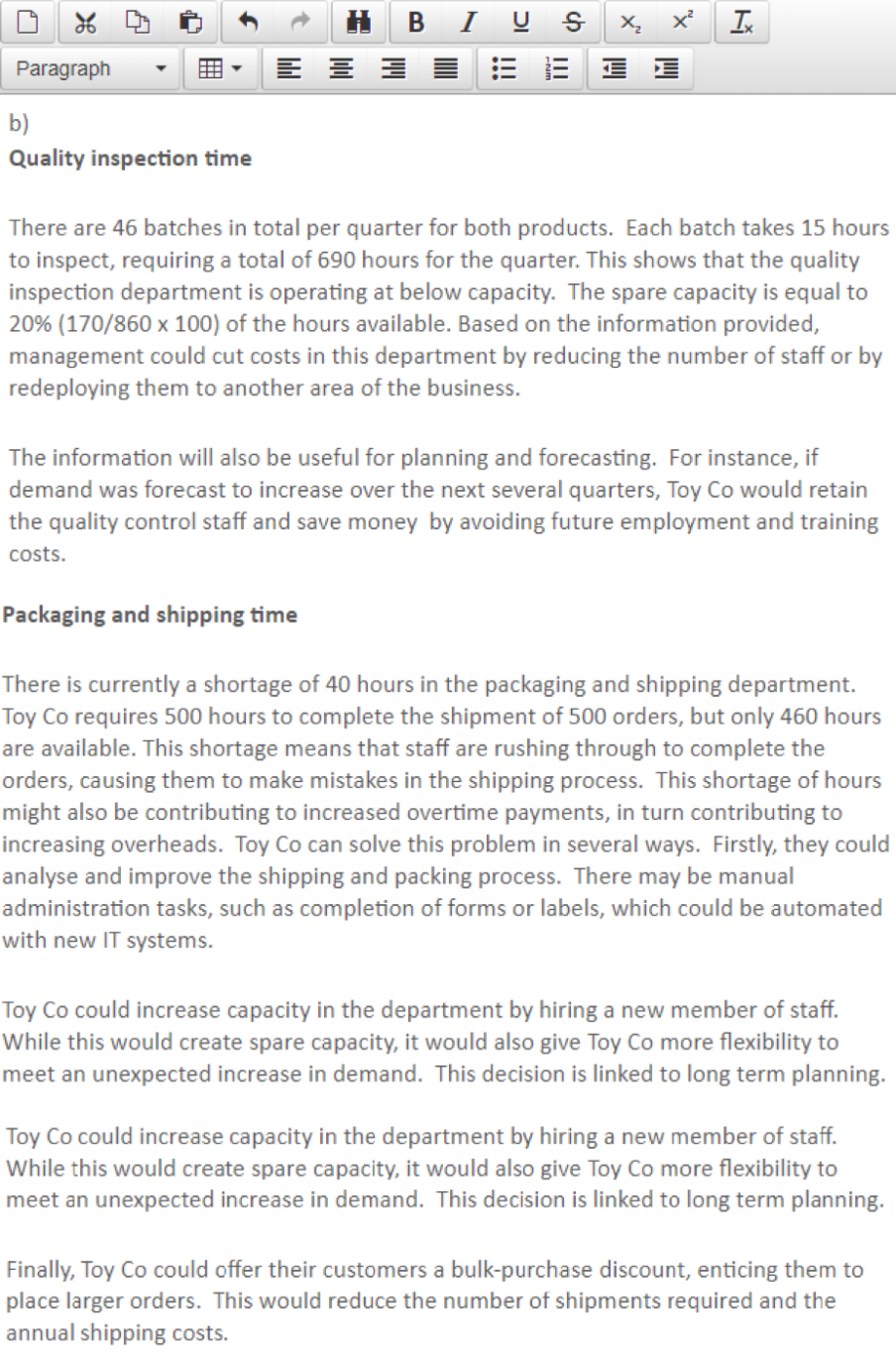

(b) Discuss the implications of your findings in (a) for Toy Co’s production process

Suggested solution:

{kind=link}

{kind=link}

Written by Steve Willis, finance and accountancy trainer