Financial analysis in Strategic Business Leader (SBL)

This article explains the approach you should take if you are asked in SBL to analyse the financial performance and position of an organisation. You will need to focus on calculations relating to factors that are strategically and operationally important for the organisation.

Reading through the exhibits

Considering what all the exhibits tell you about the organisation is particularly important for financial analysis in SBL. You will be given the financial details on one exhibit. However, you will need to draw on information from other exhibits for insights into the financial situation, to enhance your discussion of the results of your calculations.

Planning

Planning is vital for achieving a well-targeted answer. You should firstly consider how long you have to discuss financial issues. This is particularly important when the task requirements ask for a discussion of an organisation’s financial and non-financial situation. When this has happened in past exams, often answers have spent too long discussing financial issues. Not covering non-financial issues sufficiently will limit the technical marks you obtain and also demonstrate poor professional skills in failing to follow the task requirements.

You should then consider which areas of the organisation’s financial situation you need to spend most time discussing. The most important areas may be emphasised in the exhibit containing the financial information or you may be given instructions to cover specific areas. However, you may also need to use the knowledge you’ve gained from the other exhibits to help you identify what is strategically or operationally most significant. Although you need to spend enough time discussing the most important issues, over-focusing on a few figures may not provide the breadth of discussion required, so you must also ensure that your answer is sufficiently well-balanced.

You must also decide what calculations to do. The calculations you carry out should be those that give most insight into the financial situation and that you can discuss in detail. You should avoid doing a large number of calculations on which you do not comment, as you will only gain credit for calculations in SBL if you discuss the results. In addition, you will demonstrate poor professional skills if you present to the recipient of the answer a large number of calculations but do not say anything about them.

You also need to decide how to organise your answer, the headings under which the results of your calculations will be analysed. This may be indicated by the way the financial information is given to you. Bear in mind that communication skills are important, which means presenting your answer in a way that is most helpful to the recipient.

Using the spreadsheet response option

You can use the spreadsheet response option in the SBL exam if you are carrying out a number of calculations. The spreadsheet can help you carry out calculations quicker. However, marks are not awarded in the spreadsheet, so you must ensure that your analysis is completed in a word response option and each of your spreadsheet calculations is referenced and analysed within your word answer.

Discussion of results

It is never enough just to restate the results of your calculations or say that figures have increased or decreased. The recipient of your answer is looking for you to provide insight into the figures. Merely stating how the figures have moved is not helpful.

To score marks, you must explain the significance of the results of your calculations, bringing in your knowledge of what is strategically and operationally important for the organisation.

You then need to consider:

- The reasons for the results of the calculations – why have the figures changed, are the changes consistent with the results of other calculations.

- The implications and consequences of the results – what will happen if, for example, performance continues to worsen in certain areas. Considering the implications and consequences may lead on to recommendations for actions that need to be taken.

Example question

Let’s now look at extracts from the answer to Question 1(b) to the published exam for September 2020. This case study is about the Bloom Conservation Organisation (BCO), a charity that exists to protect endangered wildlife around the world. It does so by operating a wildlife park and running animal protection programmes globally. Its strategic objectives include ensuring people are better connected with nature through education and awareness of the natural world.

The BCO is particularly concerned with maintaining its income levels, as in a way it is in ‘competition’ with other charities for donations, and also because of the impact of a recession. It therefore raised the price of admission to its wildlife park in 20X1. The threats to income also mean that it is important for the BCO to control its costs effectively.

Task 1(b) asks for an analysis of the financial and non-financial performance of the BCO in the latest financial year (20X1) discussing reasons for, and implications of, the results. We shall just focus on the financial performance section of the answer.

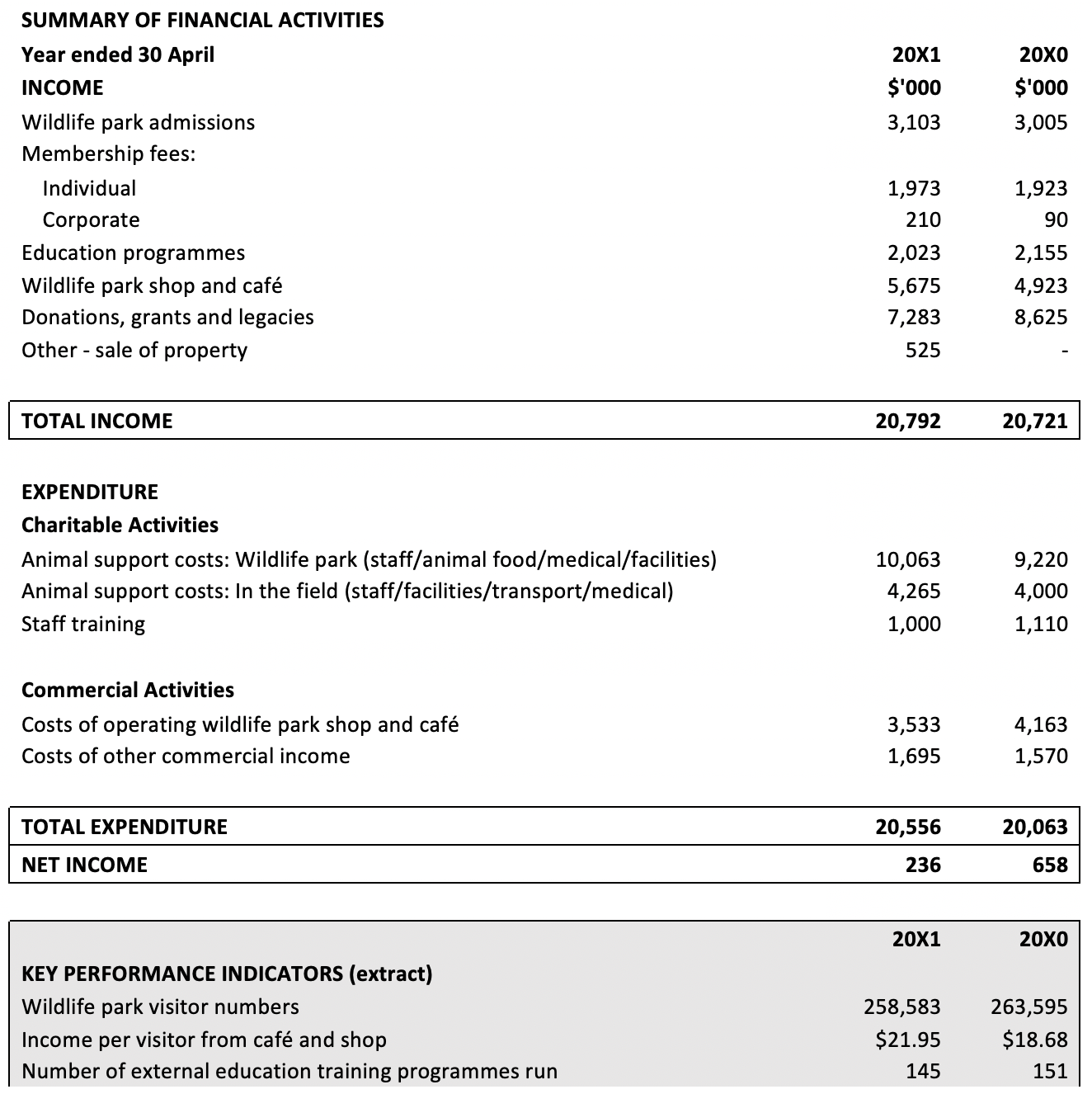

The principal exhibit relevant to this task is reproduced below:

BCO’s financial activities and KPIs – a summary of the income and expenditure of the BCO for the last two financial years (20X0 and 20X1), including a summary of its KPIs.

Click table to download a larger version

Edited extracts from the answer, together with comments are given below:

| Income from charitable activities increased by 5% in the year, much of which was as a result of admissions to the wildlife park. The increase in revenue from wildlife park admissions came from the increased price we charged this year to visitors to enter the wildlife park. However, visitor numbers to the wildlife park were down by nearly 2% (258,583, compared to 263,595 in the financial year 20X0). This is a concern, as visitors to the wildlife park are a key source of income. If visitors continue to fall, then this could have a knock-on impact on income from other sources, such as individual membership and income from the wildlife shop and café, if less visitors use our facilities. |

The significance of the increase in income here is that it is primarily the result of the rise in admission income from the wildlife park.

The answer then goes on the explain why there has been an increase – due to the cost of admissions rising.

However, a consequence of the increase in admission charges has been a fall in visitor numbers and the possible implication of this is a reduction in other sources of income. Linkage to related income shows good commercial acumen, always an important skill in a financial analysis question even if it is not given specific credit. However, despite the decrease in visitor numbers, income from the shop and café has (unexpectedly) risen significantly, which the answer therefore needs to consider and does go on to discuss as a separate issue.

| Income from running education and training programmes was 6% lower than last year. This is concerning, when considering our long-term objective of increasing our commitment to educating and training our stakeholders. This combines with the KPI showing that we ran fewer external education and training programmes in 20X1 compared to 20X0 (145 v 151) and clearly does not meet the objective. This is something we must focus on in the coming years if we are to ensure that our strategic objectives are met. |

The significance of the fall is explained by linking it to the strategic objective of educating stakeholders. The fall is explained by a linkage to the related KPI of fewer external education and training programmes.

The implication/recommendation is that this must be an area on which the BCO focuses over future years.

| Expenditure has increased in the year by nearly 2.5%, which, although not overly concerning, must be something we monitor closely. We spent significantly more on animal support costs, which increased in the year by 8%. This rise may be due to inflationary pressure on the underlying costs of resources (veterinary costs, animal feed and staff pay rises) or it could suggest we are being inefficient in our cost management procedures and not be controlling these costs effectively. This is something that we must investigate further as we may not be making the best use of our resources. We have an obligation to obtain the optimum value for money for our stakeholders and we must manage our funds appropriately. |

The increase in expenditure is expressed as being of some, but not hugely significant, concern.

The increase in overall expenditure is observed to be primarily because of the increase in animal support costs. However, the question then arises of why animal support costs have increased. The answer gives possible explanations – inflation or poor cost management – and is helpful because it suggests that more than one factor may have contributed to the decrease.

If poor cost control is a correct explanation, this has the implications that the BCO is not making the best use of resources and not achieving optimum value for money. The answer demonstrates commercial awareness by identifying this as of particular importance to the stakeholders (income providers).

| Costs of commercial operations reduced by 15% which is very positive. This may be due to fewer properties to manage (we sold a property in 20X1) or it could be because we have managed our shop and cafe more efficiently. We may be able to learn lessons from our cost management processes in our commercial operations and transfer these to our management of animal welfare costs. |

The comment on the significance does indicate the fall is of some importance.

The explanation brings in other data (the property sale) and again is useful because it points out that the change may be due to more than one factor.

The implications/actions should be seeing how these costs are being controlled effectively and applying what has been learnt to other areas of the business.

Conclusion

The most important requirement of a financial analysis task in SBL is to go beyond just doing calculations and making only superficial comments. You need to assess the importance of the results of the calculations, provide plausible explanations why the figures have changed and consider the implications and consequences for operations and fulfilment of strategic objectives. This may involve the organisation taking further action to correct problems or build on positive factors. Remember always that you should be producing a commentary which is clear and useful for the recipient of your answer, adding value to the calculations that you do.

Written by a member of the Strategic Business Leader examining team