Relevant to ACCA Qualification Papers F8 and P7

It is one of the most fundamental concepts in auditing; auditors are paid to offer an opinion. It is what they do; it’s their ‘raison d’être.’ Why then, if the audit opinion is so significant, are audit examiners continually underwhelmed by candidates’ appreciation of this topic?

This article, which is relevant to Paper F8 and P7, revisits the basic principles of forming an audit opinion and looks at how this knowledge should be applied by considering a past Paper P7 exam question.

THE BASICS

When an auditor is able to satisfactorily conclude that the financial statements are free from material misstatement they express an unmodified opinion. The complete form and content of the unmodified opinion are presented in ISA 700, Forming an Opinion and Reporting on Financial Statements. However, auditors typically use one of two well-known phrases to reflect their conclusion, either:

- ‘The financial statements present fairly, in all material respects...’ or

- ‘The financial statements give a true and fair view of...’

MODIFICATIONS TO THE OPINION

There are two circumstances when the auditor may choose not to issue an unmodified opinion:

- When the financial statements are not free from material misstatement or

- When they have been unable to obtain sufficient appropriate evidence.

In these circumstances the auditor has to issue a modified version of their opinion. There are three types of modification. Their use depends upon the nature and severity of the matter under consideration.

They are:

- the qualified opinion

- the adverse opinion

- the disclaimer of opinion.

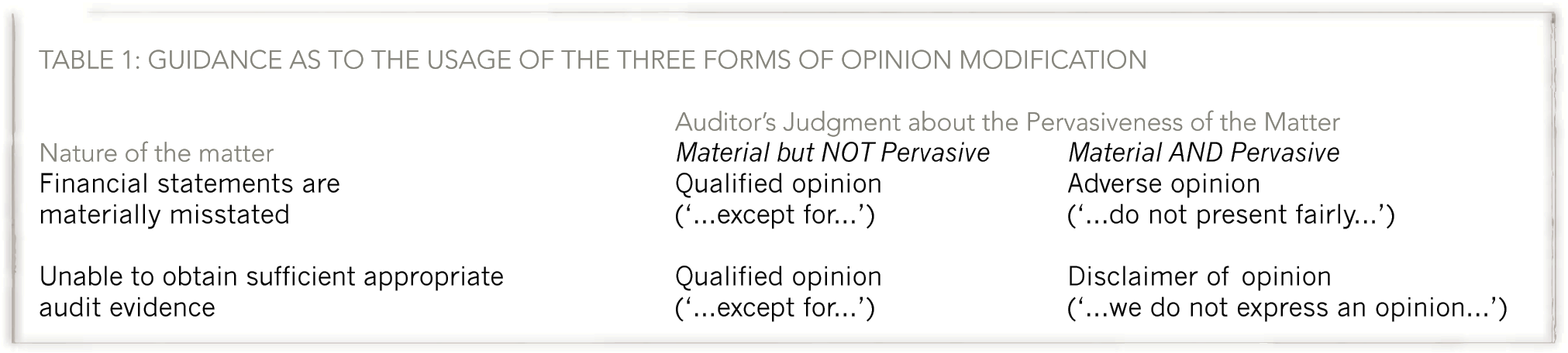

Guidance as to the usage of the three forms of modification is provided by ISA 705, Modifications to the Opinion in the Independent Auditor’s Report. This has been summarised in Table 1.

Pervasiveness is a matter that confuses many candidates as, once again, it is a matter that requires professional judgment. In this case the judgment is whether the matter is isolated to specific components of the financial statements, or whether the matter pervades many elements of the financial statements, rendering them unreliable as a whole.

The bottom line is that if the auditor believes that the financial statements may be relied upon in some part for decision making then the matter is material and not pervasive. If, however, they believe the financial statements should not be relied upon at all for making decisions then the matter is pervasive.

{kind=link}

EMPHASIS OF MATTER

Emphasis of matter (EOM) is rarely dealt with satisfactorily in the exam. This is mainly because candidates believe that EOM is linked somehow to modifications of the opinion. This is not the case: EOM and modified opinions are totally separate matters.

The purpose of an EOM paragraph is to draw the users attention to a matter already disclosed in the financial statements because the auditor believes it is fundamental to their understanding. It is a way of saying to the users: ‘you know that note in the financial statements, the one about the uncertainty surrounding the legal dispute? Well us auditors think it’s really important, so make sure you’ve read it!’.

The usage of EOM paragraphs is described in ISA 706, Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor’s Report. This identifies three examples of circumstances when the usage of EOM is appropriate:

- when there is uncertainty about exceptional future events

- early adoption of new accounting standards and

- when a major catastrophe has had a major effect on the financial position.

Of course, in all of these examples the auditor can only refer back to disclosures already made in the financial statements. If the directors haven’t disclosed a matter as required by financial reporting standards, then the auditor may conclude that the financial statements are materially misstated and modify the opinion instead.

OTHER MATTERS

‘Other matter’ paragraphs are used to refer to matters that have not been disclosed in the financial statements that the auditor believes are significant to user understanding. One usage of these paragraphs is where the auditor concludes that there is a material inconsistency between the audited financial statements and the other (unaudited) information contained within the annual report and accounts, as required by ISA 720, The Auditor’s Responsibilities Relating to Other Information in Documents Containing Audited Financial Statements.

APPLICATION TO EXAM QUESTIONS

Now that we have recapped the basic principles of audit opinions let us consider how these may be applied to an exam scenario.

Questions on audit reports in Paper P7 typically fall into two distinct types: critical appraisal of an audit report that has already been written; or explanation of how matters will affect an audit opinion. In both cases the principles affecting the choice of audit opinion are the same.

If you face a question of this nature simplify your task by asking the following questions:

- Is there a misstatement in the financial statements (ie a fraud or error)?

- Has the auditor gathered sufficient appropriate evidence?

- Is/could the matter be material?

- Does the matter pervade the financial statements?

- Does the scenario refer to a disclosure made in the financial statements concerning an uncertain future event?

Based on this approach you should be able to pinpoint exactly what form of opinion is appropriate and whether an EOM paragraph is necessary.

As an example, Question 5 in the June 2009 Paper P7 exam asked candidates to ‘critically appraise the proposed audit report of Pluto Co for the year ended 31 March 2009’. Relevant extracts from the audit report are given in Illustration 1. The full text may be downloaded from the ACCA website.

Please note that the extract is from the International version of the syllabus and refers to International Accounting Standards.

This is largely irrelevant to our understanding of the audit opinion; however, the question does deal with matters where the financial reporting requirements across different accounting regimes are broadly similar. The company in the question is a listed company.

ILLUSTRATION 1 (when this question was written, ISA 701 was examinable and disagreement with management was a reason for qualifying a report)

Adverse opinion arising from disagreement about application of IAS 37

The directors have not recognised a provision in relation to redundancy costs... and so the recognition criteria of IAS 37 have not been met. We disagree with the directors as we feel that an estimate can be made... We feel that this is a material misstatement as the profit for the year is overstated.

In our opinion, the financial statements do not show a true and fair view of the financial position of the company as of 31 March 2009…

Emphasis of matter paragraph

The directors have decided not to disclose the Earnings per share for 2009... Our opinion is not qualified in respect of this matter.

RESPONSE – REDUNDANCY PROVISION

We are not going to consider the whole wording, merely the choice of opinion. A more complete response is given in the model answer, which can be accessed via the ACCA website.

The first question to ask is whether there is a misstatement. The answer to this is clearly ‘yes’ as the report concludes that the directors have failed to make a provision when they should have. This contravenes the relevant accounting framework (IAS 37, Provisions, Contingent Liabilities and Contingent Assets). The report also clearly states that this is considered to be material to the financial statements.

Next we have to consider whether the auditor has been able to gather sufficient appropriate evidence. Once again the answer is ‘yes;’ the auditor has been able to reach a considered conclusion on the matter.

At this point we have established that there is a material misstatement. Therefore, we will have to modify our opinion. However, the final version of the modification depends upon whether the matter is pervasive or not.

There is no indication in the audit report that the auditor considers the matter pervasive. It should also be considered that redundancy provisions will only affect two areas of the financial statements: current liabilities and wages/salary costs. Does misstatement here render the remainder of the financial statements unreliable? This is an unlikely conclusion.

It therefore appears unlikely that an adverse opinion is necessary in the circumstances. A qualified (‘except for’) opinion would appear more appropriate.

Earnings per share (EPS)

The second issue is that of the EOM paragraph. Ask the question referred to earlier: does the scenario refer to a disclosure made in the financial statements concerning an uncertain future event? Clearly the answer is no. Therefore, an EOM paragraph is not appropriate.

If this is the case how should the matter be dealt with? Well, go through the same questions again. First, is there a misstatement?

The directors have failed to disclose the EPS for the year. This contravenes both IAS 33, Earnings per Share and (in the UK) FRS 22, Earnings per share, which require the basic and diluted EPS to be disclosed in the financial statements of all listed companies. There is, therefore, a misstatement in the financial statements.

Next we consider whether the matter is material. The clarified ISA 320, Materiality in Planning and Performing an Audit requires the auditor to consider the informational requirements of the users. EPS is a vital investor analysis tool and can therefore be considered material by nature. For listed companies, it is a requirement of financial reporting standards that EPS is disclosed with prominence in the financial statements. There is therefore a material misstatement in the financial statements.

Finally the auditor should consider whether the matter is pervasive to the financial statements. The lack of disclosure of the EPS ratio is unlikely to render other elements of the financial statements unreliable; it is an isolated error. In this instance a qualified opinion should be given on the basis of a material misstatement of the financial statements.

APPLICATION TO THE PAPER F8 EXAM

The concepts considered above are equally as relevant to the Paper F8 exam. However, the wording of the questions to date has been slightly different from the Paper P7 exam. So far candidates have been provided with short scenarios and asked to either state or explain the effects of the matters on the audit report. The approach discussed above may be applied in the same way to these questions.

The matters considered so far (in the December 2007 and December 2009 exams) include: a failure to depreciate non-current/fixed assets, an auditor not being able to attend the year-end inventory/stock count, and a failure to disclose a contingent liability in the financial statements.

Candidates should also prepare for questions requiring them to define or explain the terms referred to above.

This style of requirement is illustrated in Question 2 from the June 2009 exam paper.

CONCLUDING THOUGHTS

Audit reports are a fundamental part of the auditing process and are therefore significant for audit students at all levels. This will continue to be a regular exam topic.

If you do struggle with these questions it is NOT a good strategy to suggest every possible form of opinion hoping that one of them will be correct.

Auditing requires critical appraisal, the use of professional judgement and the ability to offer a reasoned opinion.

By asking yourself a series of simplified questions you will go through a critical thought process that allows you to come to your own conclusion and, more importantly, offer your own opinion.

This will undoubtedly allow you to present an answer that stands out from the others.

Simon Finley is an audit subject specialist at Kaplan Publishing